Fintech in DACH region of Europe is the quiet revolution and the region has attracted progressively more of the global funding pie since 2017, emerging as a genuine rival to Asia and North America for fintech VC dollars. Click here to read

Fintech Saudi Arabia is ready for take-off and Saudi Arabia is one of the world’s fastest-growing fintech hubs. And as the region’s largest economy the potential to become a global reference point for fintech across the Middle East and North Africa is real. Click here to read.

Fintech Mundi’s annual Nordic Insight Briefing focuses on ‘Digitalization’s Next Act’. At the Mastercard Lighthouse event in Tallinn we discussed what’s next for the region which continues to produce world-beating solutions, and incubating industry giants. Read here about the key opportunities in store.

findexable and Fintech Mundi are delighted to announce the launch of our inaugural Diversity for Growth Report, in partnership with fintech firms Chargebacks911 and Global Processing Services (GPS).

The report is the cornerstone of our Fintech Diversity Radar, the world’s first global platform to accelerate diversity in fintech.

In the report, we uncover systemic underrepresentation of women in the fintech industry, including:

A new 1% club: Only 1.5% of the best funded private fintech firms globally are founded solely by women and receive just 1% of total fintech venture funding.

No seat at the table: Women make up 11% of all board members and 19% of company executives.

West is no longer best: Asia has the highest proportion of female founders at 7.7%, and Africa and the Middle East are the leading regions for the proportion of female CEOs.

The tech gender gap: Less than 4% of women globally hold the title of Chief Innovation or Technology Officer.

A (pandemic) year in the making – the 2021 Global Fintech Rankings

#PoweredbyMambu, after a year of crunching the numbers, interviews with fintech ecosystems around the world – we’re thrilled to bring you the second edition of the Global Fintech Rankings – the only global rankings of fintech ecosystems now covering 264 cities and over 80 countries (including 50 newly crowned fintech hubs).

This year we’re celebrating the winners and unpacking what’s happening in fintech and fintech ecosystems around the world during a notably tough year. Download the full report here to see who’s new.

While many of the Top 20 remain unchanged – there are some surprises. Tel Aviv joins the top 5 for the first time while Berlin’s rise up the rankings is making the city a genuine contender for Europe’s fintech crown.

A joint undertaking between Fintech Mundi and findexable and with FCG, Huawei and Mastercard, the report seals the success of the Nordic fintech community, which stands strong, with investors and innovators hard at work across the space.

The region’s early success at moving away from cash, its embrace of collaborative models for the development and distribution of innovative financial services long before fintech became every bank’s favourite bandwagon, and commitment to digital services have created the foundations for a thriving fintech ecosystem.

Fintech exists to solve global problems. Of access – such as in emerging markets where banking economics stop the poor from getting a bank account. Of speed – where old infrastructure slows the sending of money, receipt of payments or makes international trade difficult. Or of cost and convenience – by making it easier to pay, or cheaper to borrow. There’s another problem too. An industry founded on principles to make the world better, needs a global index to track progress, and benchmark its success.

This is the vision of the Global Fintech Index of which I am a proud Ambassador. The City Rankings Report 2020 is the first glimpse of what the Index algorithm is designed for. To identify emerging hubs, fintech com¬panies and trends. To promote growth and adop¬tion of progressive, inclusive financial services everywhere.

Together with our Partners we’re building a global coalition to promote the values of fintech. We hope you’ll join us in our mission too.

Fintech

Mundi has teamed up with long-standing partner MagnaCarta Communications and a

coalition of other global partners to identify, compare and track the

development of fintech everywhere – even in the furthest corners of our planet.

Launching

in October, the Global Fintech Index, presented under the banner of Findexable,

will be the first fully global index of cities ranked by fintech activity.

Fintech Mundi’s Susanne Hannestad explains the needs of the fintech sector in the Nordics and how accurate, tangible data can help raise the Nordics’ status as a hub of fintech innovation globally.

The Nordic and Baltic region has all the building blocks to generate wealth and opportunities and is punching above its weight in terms of producing unicorns, moving from start-up to critical scale-up phase and it leading the rest of Europe on Open Banking and PSD2 progress. Results from the fourth Nordic Fintech Disruptors Report launched during Money 2020 in Amsterdam finds confidence in abundance at 68%, 14% up from 2018.

The report produced by MagnaCarta and Fintech Mundi in partnership with Mastercard and BDO, is a comprehensive review of the current position and future trends in Nordic and Baltic fintech. It features extensive interviews with banks, fintechs, regulators, accelerators and leading innovators, alongside the results of an industry-wide survey.

Although more than half the survey respondents believe that the Nordics and Baltics will dominate the fintech landscape after 2020, the confidence is tempered with realism and a recognition of key challenges. 67% of respondents feel the region needs greater access to investor capital to realise its potential (24% higher than 2018), while over half believe that greater openness to partnering will help the region compete on the global stage.

Against this background, this year’s report is more of a manifesto, setting out a vision for how the region can fully realise its strengths and take full advantage of the new era of integrated digital finance. Much of the answer still lies in viable, effective partnerships and a better connected fintech ecosystem which offers the best chance to:

Attract skills and talent required to continue developing the marketplace

Bring more customers on board to create sustainable businesses

Serve and support new businesses to create more winners

Fertilise new ideas at scale and shorten times to profit

Grow the region’s reputation to create a virtuous circle for success

“Since we started the research in 2014 we have seen a region that has

outperformed many in developing and nurturing fintech innovation but true

collaboration and trust across the ecosystem remains an issue which has to be

addressed if the region is to fulfil its potential as a global fintech hub, ”

comments Simon Hardie,

author and publisher of the report.

The report is a call to arms for banks, investors, regulators, public bodies

and for the fintechs themselves,” says Susanne

Hannestad, CEO of Fintech Mundi, a prominent Nordic based

fintech accelerator. “The Nordic and Baltic regions are ideally placed to

out-perform their peers in Europe, but only if we can find a more effective way

to work together. We are not there yet.”

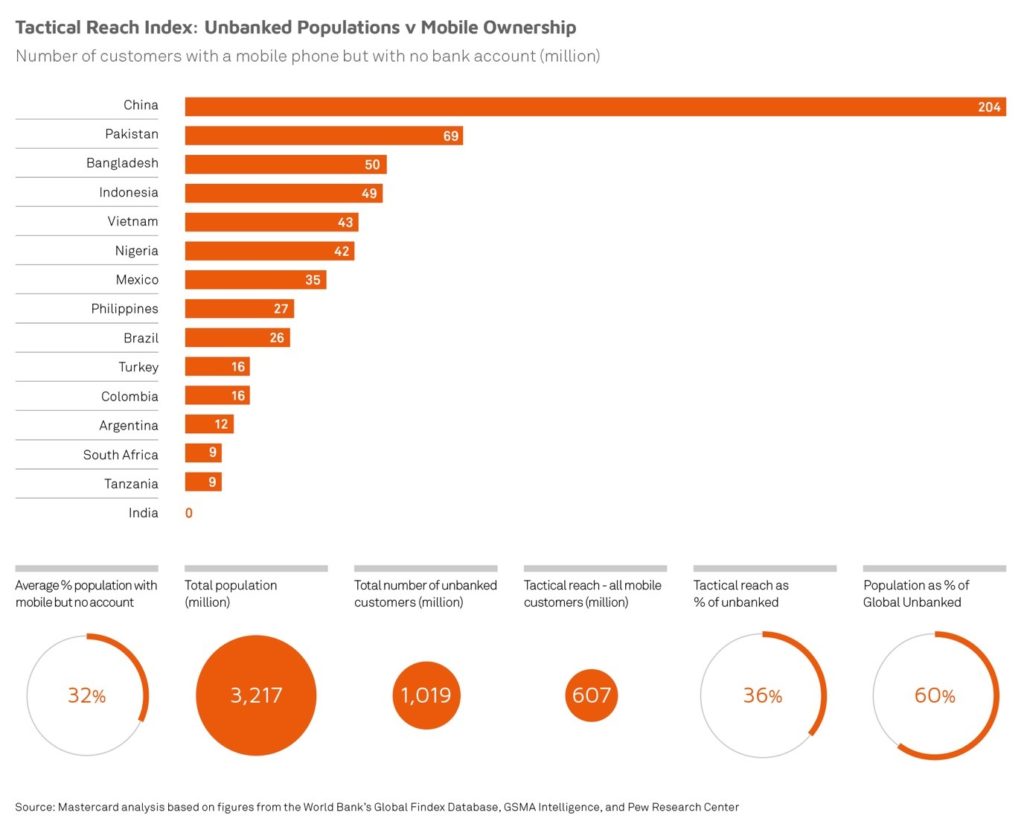

A new report from Mastercard confirms the power of mobile technology to improve financial inclusion. The research shows that 15 countries account for over 60% of the global unbanked population, where 607 million people have a mobile phone, but do not yet have a bank account. Mobile technology could therefore provide them with immediate access to the benefits of financial inclusion.

In 14 of these countries, the number of people with a mobile phone outnumbers the number of people with a bank account by several million (rising to 204 million in China). The only exception is India, where more people have a bank account than a mobile phone.

However, the report emphasises that simply providing access to

financial services is not enough to address financial exclusion. To achieve any

real impact, people also need to become active users of financial products. Globally,

20% of people with a bank or mobile money account have not used it for more

than a year, and many more people only ever use their account on an occasional

basis.

In the absence of banking services, or if financial products are rarely

used, people inevitably turn to informal providers, such as neighbourhood

savings clubs, local money lenders, and unlicensed remittance services. Most

people on low incomes tend to be experienced users of these informal financial

products, and to have intricate and well-ordered financial lives. However, they

do not have legal protection, face significant risks, and may pay more for a

vastly inferior product.

As the report says, “the battle for inclusion is not about

creating completely new behaviours or building entirely new markets. Nor is it

about providing simple access to the financial mainstream. It is about how bona

fide players and regulated providers can do a better job of out-competing the

informal sector.”

Another important consideration is a deep gender gap, which could

be exacerbated if mobile and digital technologies were to become the

predominant delivery channel for financial services. In developing countries,

for example, there is already an eight-percentage-point gap in account

ownership (67% or men have an account compared to 59% of women). This gap

extends to double-digits in many countries, such as Morocco and Peru, and

reaches 30% some countries, like Pakistan and Bangladesh. Women are much less

likely to have made or received a digital payment, more likely to have used

informal financial products, and less able to come up with emergency funds in

the face of an emergency.

The report, Unravelling the Web, was commissioned by Mastercard

and produced by MagnaCarta Communications. It was launched at the Financial Inclusion Summit in Oslo on 28

March 2019, where speakers included Ann

Cairns, Vice-Chairman and President International Market of Mastercard, Greta Bull, CEO of CGAP (World Bank)

and James Mwangi, CEO of Equity Bank

Kenya.

We use cookies to optimize our website and our service.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.